Can Europe Turn Its Frugal Savers into Investors?

The European Union wants to encourage the region’s cautious savers to invest more.

- The EU has launched plans for a single, integrated capital market that aims to mobilize the region’s huge savings pools.

How to persuade Europe to invest rather than save?

That is the challenge European authorities have set themselves: Can they turn a continent of frugal savers into something closer to the U.S., where a greater percentage of disposable income is invested into capital markets and start-ups, rather than squirrelled away in low-yielding bank deposits?

Changing a risk-averse culture can be hard, but that is one of the tasks set for the EU in the 2024 report by former Italian Prime Minister Mario Draghi, which considered how to integrate Europe’s capital markets to better channel household savings towards productive investments.

The region certainly needs more investment. Europe’s growth lags the U.S., it has an aging population, and industries are struggling in the face of U.S. tariffs and cheaper Chinese imports. One proposed fillip put forward by the European Commission is the Savings and Investments Union (SIU), an integrated capital market that could help channel household savings into potentially higher-returning products that support SMEs and innovative companies.

The SIU’s ambitions include breaking down barriers for product distribution across borders while reducing operational hurdles facing asset managers. They also encourage the creation of new tax-friendly savings pools and target the practice of gold-plating regulations, whereby national regulators add more stringent provisions to Europe-wide securities rules.

“Regulations and rules (in Europe) around what individuals and pensions can invest in need to keep up with the changing investment universe,” said Vai Rajan, Managing Director and Head of EMEA Private Wealth at EQT.

Europeans are big savers, small investors

Europeans saved almost €1.4tn ($1.6tn) in 2022, well above the €840bn saved by Americans, according to the Draghi report. Yet just 17 percent of EU households’ wealth is in listed shares, bonds, mutual funds and derivatives; in the U.S., as much as 43 percent is in financial securities.

This difference helps explain why Euro-area net household wealth grew by just 55 percent between 2009 and 2023 versus a whopping 151 percent in the U.S. Lower levels of household investment are also a contributor toward Europe’s shallower capital markets where even promising businesses often struggle for funding.

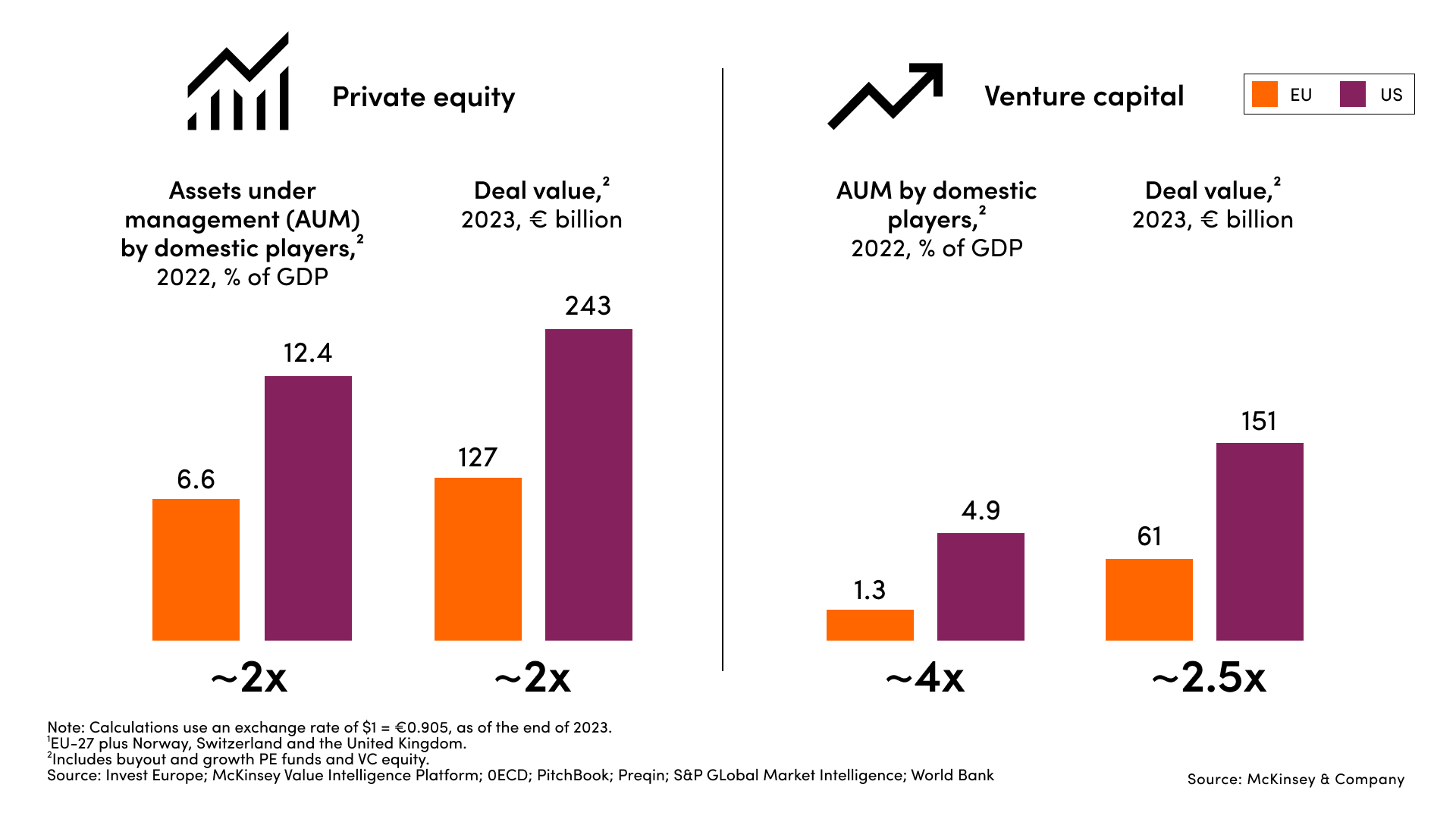

One related metric: assets under management at private equity and venture capital funds equate to about 8 percent of Europe’s GDP compared with 17 percent in the U.S., according to McKinsey & Co.

Europe's private market sector compared to the U.S.

That has helped lead to some stark outcomes: In the past 50 years, the U.S. has created 241 companies from scratch with a public valuation exceeding $10bn, according to research by Andrew McAfee at MIT. The EU has generated just 14, of which four alone are Swedish. No surprise that tech startups like Swedish payments firm Klarna or Ireland’s Flutter Entertainment opted for listings in the U.S. where investor interest and liquidity is greater.

How to challenge the status quo

Among the SIU’s goals is to challenge how Europeans plan for retirement, by encouraging people to save via private pensions in addition to state provisions.

Pension systems that are statutory and give savers little incentive to be involved in investing decisions, unlike 401(k)s or IRAs in the U.S., add to Europeans’ lack of a systemic push, according to Christian Hecker, CEO and co-founder of Trade Republic, a Europe-based digital banking and savings platform with more than €150bn in customer assets.

“Investing is often mistaken for speculative trading, not long-term saving…this creates a dangerous paradox: we face a massive pension gap, yet participation in the capital markets remains low,” Hecker says.

In this regard, Sweden’s private pension system is seen as a model for others. Thanks to the self-directed and tax-efficient ISK plan, combined with a school curriculum that includes financial education from the first grade, Swedish households invest as much as 51 percent of their wealth in stocks – more than double the average in the Euro area, according to the European Savings Institute.

Private market accessibility

Another effort is the rollout of private markets funds accessible for household investors who don’t have the millions of euros usually required to invest in the alternative asset class. Such funds go to the heart of the Commission’s plan to channel savings into the world-leading companies of tomorrow.

The European Long-Term Investment Fund (ELTIF) framework, which was updated last year to remove minimum investment requirements, is one route for alternative asset managers to create and market funds once reserved for institutional investors, to ordinary households across the EU more seamlessly.

“The advances in the ELTIF regime have given retail investors a much easier way to access private markets and for distributors to reach them,” Rajan said.

“Even so, we still need financial education in Europe so savers understand the value of investing, and regulations also need to address the changing risk-reward profile of the asset class,” Rajan added.

Learning from past lessons

There’s no doubt that harmonizing rules across a 27-nation bloc where members sometimes prioritize domestic interests over a unified approach will be challenging. The EU struggled to implement the integrated banking system it announced in 2015, or to progress on the Capital Markets Union, an earlier iteration of the savings and investment union.

Regulators can be slow to respond to the EU’s evolving investment landscape, notes Rajan, using the example of the recent advent of retail-focused evergreen private markets funds. Investor suitability thresholds have long been linked to liquidity, so private markets funds that include a lock-up or redemption window are automatically labelled high risk, regardless of the quality of the underlying asset.

“With strong historical returns from private markets, combined with shrinking and concentrated public markets, characterizing the riskiness of these investments needs to become more nuanced,” Rajan says.

ThinQ by EQT: A publication where private markets meet open minds. Join the conversation – [email protected]

MoreInsights

Exclusive News and Insights Every Month

Sign up to subscribe to the EQT newsletter.