What is a Private Equity Fund?

Learn the essentials of private equity funds—how they are created, raised, structured, and managed. This guide provides an overview of the lifecycle of PE funds, from raise to wind-down, and their governance.

- PE funds are created to pool capital from investors to acquire, improve, and sell businesses to create long-lasting value.

Private equity (PE) funds are major players in the world of finance, known for their ability to drive growth, create value, and generate substantial potential returns for investors. Their effectiveness is why in 2025 there was more than $22tn in assets under management with private markets firms.

For those looking to understand what a PE fund is, this article dives into the essential aspects, from the reasons these funds are created to their fundraising processes, governance structures, and lifecycle stages.

Why are private equity funds created?

PE funds are created to pool capital from investors to acquire, future-proof, and ultimately sell businesses for a profit. Whereas a public company listed on the stock market is held accountable to its shareholders every quarter, PE funds can invest in portfolio companies and develop them with an undiluted focus on the long-term success of those businesses.

Such funds first emerged in the mid-twentieth century to capitalize on private sector growth opportunities, often using borrowed money to improve investment returns. They typically focus on companies where they can make a substantial impact through operational improvements and new market expansion.

How are private equity funds structured?

A PE fund is typically set up as a limited partnership with two main parties:

- Limited Partners (LPs): the investors who provide most of the capital in the fund are known as the LPs. These are typically institutional investors (for example, pension funds, insurance companies, sovereign wealth funds) or high-net-worth individuals, though increasingly, there are PE funds targeting retail investors as well.

- General Partner (GPs): the private equity firm that manages the fund is known as the GP. The GP is responsible for the fund’s operations. The GP will also invest in the fund, ensuring an alignment of interest to LPs. Traditionally, this co-invest level has been in the region of 1-5 percent, though occasionally commitments are much higher.

Beyond simply being a tried-and-tested model, this structure is used for a number of reasons. Firstly, there are tax benefits to setting up as a partnership, not a corporation. Secondly, it allows LPs to give control of funds to GPs, who can use their expertise in private equity to make investments. Thirdly, a limited liability setup protects LPs, who are not directly involved in fund management.

The funds are typically created using a closed-end model meaning investor capital is locked up for an agreed minimum timeline. This can be upwards of a decade. One key advantage to this model is that the GP can invest in illiquid assets, such as private companies, without worrying about investors suddenly wanting their money back.

For overseeing the operations of the fund, the GP earns management fees. The industry standard has been around 2 percent per annum, but this number has trended lower over time. However, these fees are complemented by ‘carried interest’, a share of the profits on the fund’s investments – typically 20 percent of any gain, though this is subject to first hitting an agreed minimum return target.

How are private equity funds raised?

PE funds typically raise money from institutional investors (for example, pension funds, insurance companies, sovereign wealth funds) or high-net-worth individuals. The process for raising funds usually follows a standard blueprint.

- Pre-marketing: between 6-12 months before the official launch of a fund, the fund managers will test investor interest through informal discussions to gauge investor appetite.

- Roadshow: the PE firm’s executive team will set up a series of presentations to promote their new fund to potential investors.

- Due Diligence: investors undertake legal and commercial due diligence on the fund. Checks can include track record analysis and ESG review.

- Capital commitment: investors sign agreements to commit capital to the fund.

- Closing: wrapping up the fundraising process usually happens in stages. There may be an initial closing when a certain threshold (around 50-75 percent of target funds) is met, and then subsequent closings to allow additional investors to join.

Naturally, the success of a fundraiser is affected by the broader economic environment, and competition between GPs for investment capital.

In recent years, there has also been a growth of perpetual funds called evergreen funds targeted at retail and affluent individual investors. These funds are marketed through pension and investment platforms and continuously accept new capital. They are more liquid than traditional closed-end funds and allow periodic redemptions so investors can withdraw capital.

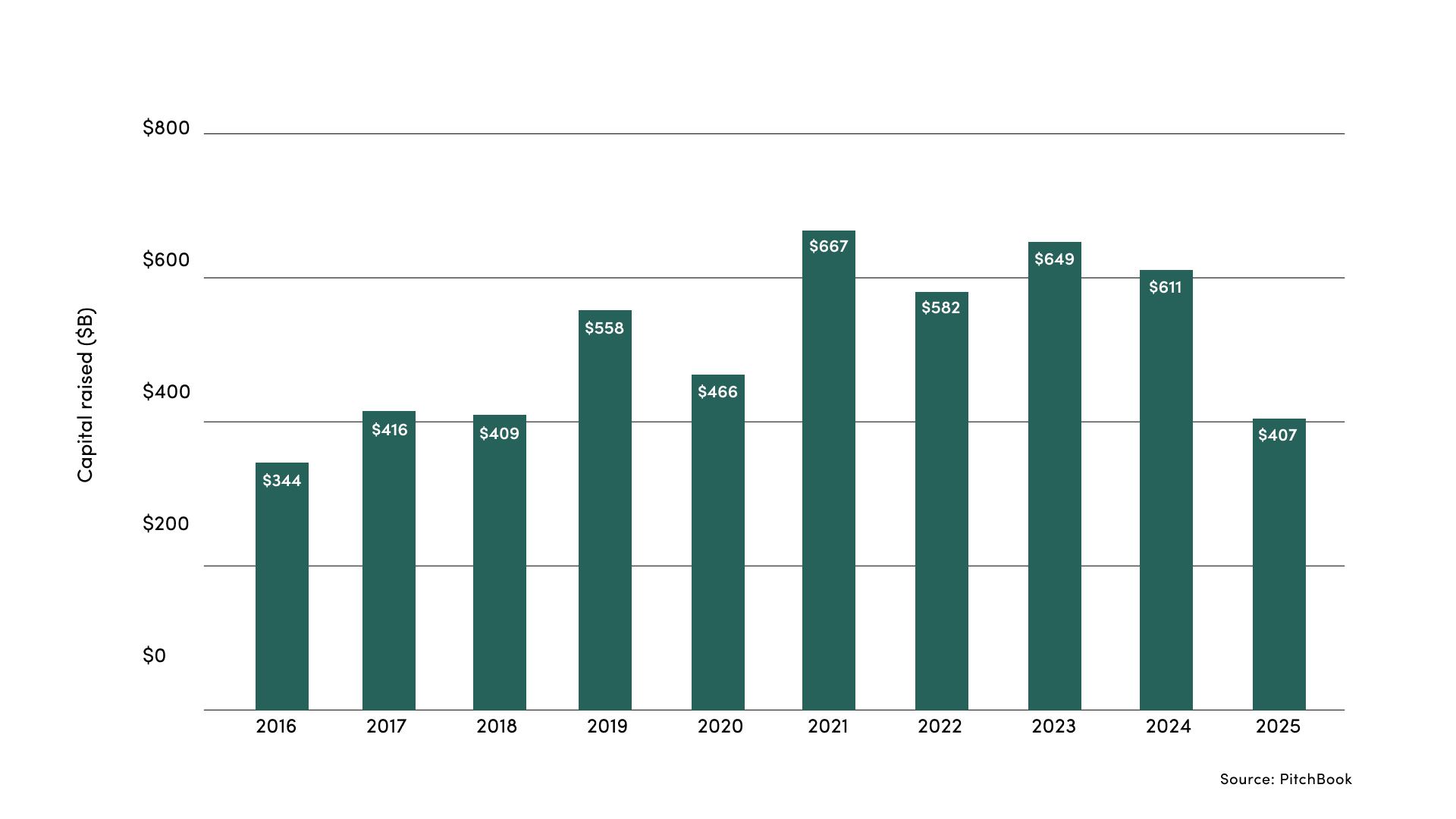

PE fundraising levels in recent years

How do private equity funds work once set up?

Once a PE fund is set up and capital committed, the focus shifts to executing the investment strategy and managing the portfolio companies. We can treat these separately for simplicity’s sake:

- Investment period: usually lasting between 3-5 years, this phase sees the GP actively seeking out and acquiring target companies. The GP leans on its industry expertise and networks to find investments that align with the fund’s strategy. This process is rigorous and involves a lot of due diligence, including financial and market analysis to ensure that a target company has growth potential.

- Active management: once a target company has been acquired, the GP will take an active role in managing and improving it. There are many strategies at a GP’s disposal, but the most common include operational improvements, financial restructuring, replacing senior staff and providing strategic guidance to company management.

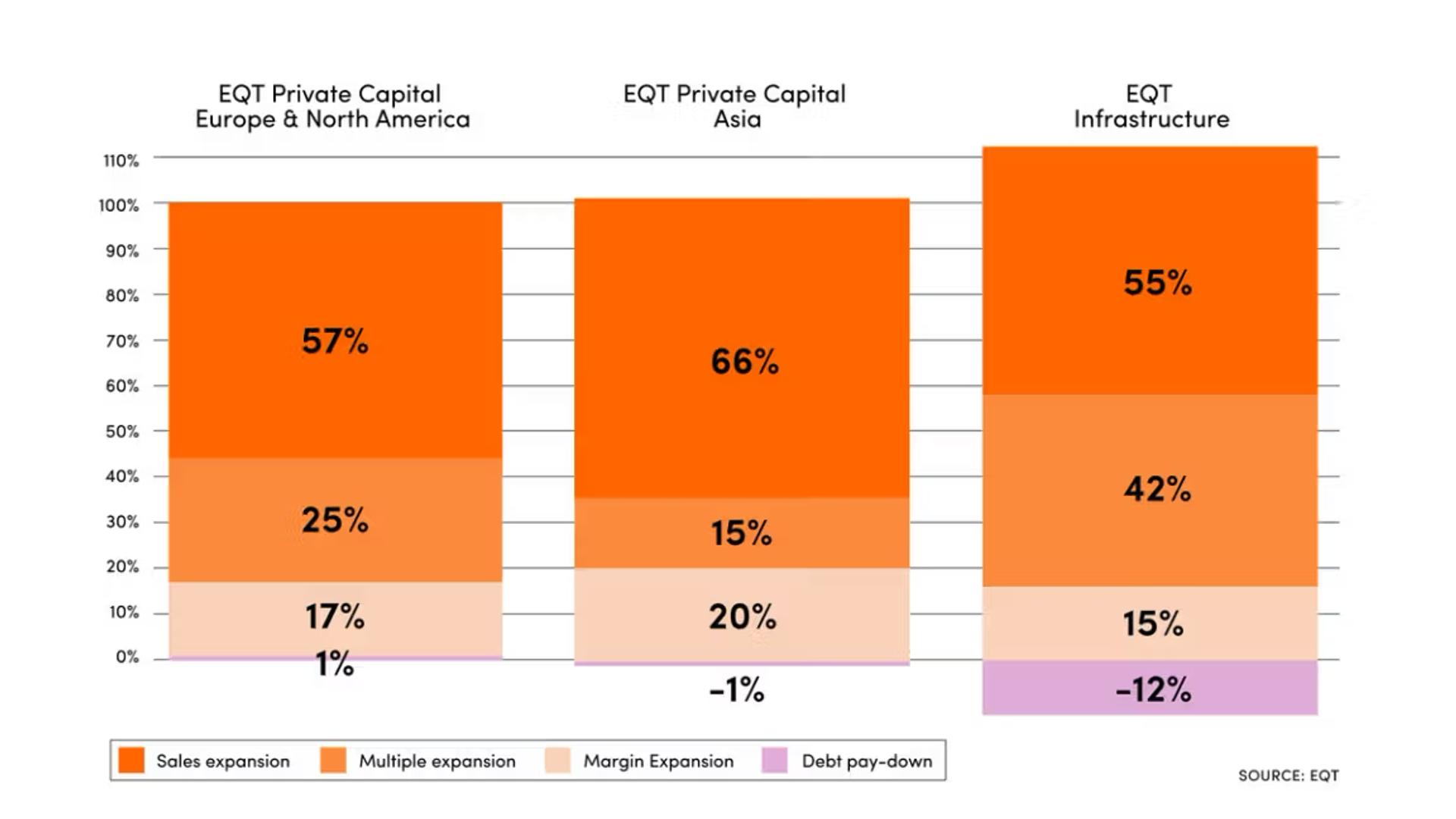

Ultimately, the goal of the GP is value creation. GPs typically look at several areas where they can improve a company’s operating and financial performance: Sales growth and margin expansion are pursued through multiple strategies, including geographic expansion, new products, acquisitions and strategic re-orientation.

Analysis of EQT’s private capital portfolios has found that the single largest creator of value is growing a company’s sales, a strategy that sometimes requires refocusing a firm’s operations and challenging the status quo to maximize growth.

By improving the operational and financial performance of the fund’s portfolio companies, the GP aims to create a future-proofed business that will be attractive to potential buyers.

Sources of value creation

How are private equity funds governed?

The governance of a PE fund is organized to ensure transparency, accountability, and alignment of interests between the partners. Here’s a general overview of the actors involved in the governance of the PE fund.

- The role of GPs: we’ve already learned that GPs are responsible for the day-to-day operations of the fund. This includes making investment decisions and creating value by working with portfolio companies, but it also includes providing regular updates to LPs on the fund’s performance.

- The role of LPs: they provide the majority of a fund’s capital. They rarely get involved in day-to-day operations though can play an important role in terms of oversight and governance as members of Limited Partner Advisory Committees (LPACs).

- LPACs: these committees are made up of LP representatives and function as advisory councils to the GP. They meet regularly to review fund performance, oversee conflicts and governance matters, and ensure the GP’s activities align with the interests of LPs.

ThinQ by EQT: A publication where private markets meet open minds. Join the conversation – [email protected]