Surfing the Wave: Preparing Firms for an IPO

Our experts discuss IPO planning for portfolio companies and the measures used to judge success

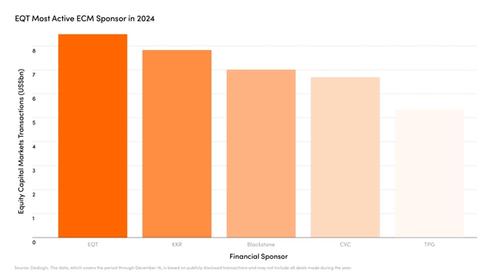

- EQT was behind Galderma‘s public listing, one of the largest IPOs of 2024.

Laying the groundwork for an initial public offering (IPO) is no small task, taking months – perhaps years – of careful planning. At EQT, planning can begin long before the firm acquires the company it is seeking to float.

“I have a good overview of our potential IPOs stretching ahead to 2028,” Magnus Tornling, Global Head of Equity Capital Markets at EQT, says. “It’s really important to be prepared when the IPO window opens.”

On paper, the geopolitical instability of 2024 should have made it a tough year for public markets, yet leading stock indices were touching all-time highs by early December. Meanwhile, the tepid IPO market of the first quarter had gathered steam to close the year strongly, heated by an unusually large number of private equity-backed floats.

According to a report by EY, there were 1,215 IPOs globally in 2024, compared to 1,415 in 2022. The report said that venture capital and PE-backed floats generated 46 percent of IPO proceeds last year, up from just 5 percent in 2022. Some 12 of the 20 largest IPOs were PE-backed.

Among the top five was the IPO of Galderma, a leading Swiss dermatology company, which undertook the largest listing in Switzerland since Swisscom in 1998. In March last year, Galderma, an EQT portfolio company, floated on the SIX Swiss Exchange. By the end of 2024, its stock price had nearly doubled.

Largest PE-Backed IPOs Since 2016

Source: PitchBook

An IPO is the start of the exit process

“We don’t view an IPO as an exit event per se – it’s merely the start of the exit process,” as EQT’s approach is to gradually sell down its ownership stakes in newly listed companies, Tornling explains.

“If a company’s stock trades poorly after its IPO, liquidity dries up, and it becomes much harder to monetize the position. This creates the risk of being stuck in a public market for a long time, which is not in the interest of our investors.”

Once an IPO is considered the best exit route, EQT executives and the management team at the portfolio company enter preparatory discussions.

“Sometimes, it’s us folks at EQT who believe the time is right, but the management team has reservations,” Tornling says. “So our job is to convince them it’s time to launch. Of course, the opposite can also be true.”

Lennart Blecher, Deputy Managing Partner and Chairperson of EQT Real Assets, says a key step in IPO planning is a careful analysis of the portfolio company’s management team. “Public markets require unique skillsets,” he says, “so when we decide to IPO, we undertake a detailed review of the management team and its capabilities.”

Blecher gave the example of Kodiak Gas Services, the US contract compression company that EQT floated in June 2023, and its Chief Executive Robert McKee, whom Blecher described as “just the right kind of person to lead a company in a public market”.

However, as with many portfolio companies preparing to IPO, EQT needed to help Kodiak add investor relations functions and beef up other parts of its management team.

“The entire management team needs to be capable of handling public markets processes like earnings calls and analyst meetings, and the added scrutiny that comes with that,” Blecher says.

“Then there are the public reporting requirements and financial controls required for regulatory compliance, some of which will be specific to a given industry. This is all new to companies that might always have been private, and may require significant additional resources.”

Lining up bankers

As the company moves closer to the home straight of the IPO, the next step is to find the right banks to sell the company’s stock. Then there will be potentially dozens of meetings with investors and analysts where management needs to sell the company and its story – and that story has to be compelling to stand out from the crowd.

Carefully structuring stock awards for members of the management team helps with performance in the 12 months after the IPO, Tornling says. This might involve applying a higher ‘fair market’ price to a portion of the awards, and releasing this stock only if the price reaches or exceeds the fair market price for more than 30 days.

For EQT, the definition of a successful IPO is one that creates two additional monetization events in the 12 months after the float. “To do that, the IPO needs to be priced and allocated in a way that invites trading in the aftermarket,” Tornling says.

“We want to be long-term successful, not short-term greedy. We always try to leave money on the table at IPO – we’re very careful not to push the price too high – so people get to earn money on our deals and come back to us for the next one.

I’m not saying we get it right every time, of course. But we work really hard with our portfolio companies on their projections and targets with the aim of firstly, giving the IPO price a pop, and then, perhaps more importantly, ensuring they deliver on their promises. It’s not just about one-quarter of good results: we want to beat targets for three or four consecutive quarters. That gives faith to the market and helps us to exit the company faster.”

Tornling believes that EQT’s own journey to IPO puts it in a stronger position to support portfolio companies when doing the same. “We know how much stress it can cause in an organization,” he says. “So we always aim to reduce the pressure on the management team, because their most important job is to run the company. And it’s likely the only time they will take part in an IPO, whereas we do a few IPOs a year.”

As for 2025, Christian Sinding, Chief Executive of EQT, said in January that the firm had “several companies that are ripe for exit” in the coming year, adding: “It depends on market conditions, but we are prepared to surf the wave.”

ThinQ by EQT: A publication where private markets meet open minds. Join the conversation – [email protected]