Old Strengths Are Fueling Europe’s New Decacorns

EQT partner Sandra Malmberg sits down with ThinQ to discuss how European founders are building with more ambition than ever – and doubling down on some of the continent’s structural advantages.

- After decades of lagging, European tech is starting to look competitive, especially in AI applications and deep tech.

European tech is acting like it has a point to prove. In the 50 years through 2024, the U.S. created 241 public companies worth more than $10bn, while Europe created just 14. But 2026 is already presenting signs that the next 50 years could look very different.

From Ineffable Intelligence, an artificial intelligence lab founded by DeepMind alumnus David Silver, raising a $1.1bn seed round, to Swedish AI-native software platform Lovable doubling annual recurring revenue to $400m in four months, and London’s ElevenLabs hitting a $11bn valuation, the continent is having a big start to the year.

There are a number of factors compounding this momentum. Europe’s historic advantages are beginning to count for more in the age of AI, as more capital from North America flows into the region and the talent exodus to the U.S. shows signs of reversing.

“Where talent goes, opportunity flows,” says Sandra Malmberg, a Stockholm-based partner at EQT Ventures, EQT’s venture capital arm, reflecting on why now might be an increasingly attractive time to build in Europe.

Building for users

Much has been made of the fact that the vast majority of frontier AI research is happening at U.S. and Chinese companies. However, this GPU-intensive work is eye-wateringly expensive and – when it comes to building the tools that companies actually use – Europe is very much in the race, thanks to some distinct talent advantages.

Malmberg says that Lovable’s rapid growth has been built not just on engineering excellence, but a Nordic flair for design, brand and user experience that has helped create global success stories in tech.

“Early successes that we have in Sweden within consumer have been design-driven brands, for example, Spotify and Klarna. User experience has always been a way to disrupt markets. That’s kind of in our DNA in the Nordics,” she says, adding that, while other companies saw the potential for AI software development, Lovable’s brand and UX helped it cut through.

“What they did really well was how they packaged the technology to make it available to a broader mass of people. They just made it super simple, which enabled them to get adoption. Then their brand and their name also played a big role in their success.”

Malmberg says this was underpinned by Sweden’s technical talent, emerging from universities like Stockholm’s KTH. The strength of Europe’s research institutions is also placing it in a strong position within other frontier deeptech sectors.

“In photonics, quantum and fusion, if you look at the talent base [in Europe], it’s highly globally competitive,” she argues.

New tech built on old strengths

This research excellence is complemented by a strong European manufacturing base in sectors including defense and automotive, which are increasingly investing in cutting-edge tech like robotics and AI automation.

“You have talent that has done industrial scaling at incumbents. It's basically about merging the world of scale-ups and startups with this talent from incumbents,” says Malmberg. “You have talent that has built up large production sites, and these are skills that are very much needed on the journey to scale.”

She adds that a company like Parloa, a Berlin-based agentic AI customer service tool and an EQT portfolio company that hit a $3bn valuation in January, is also benefiting from its home market’s strong tradition of B2B selling.

“They’re using the German DNA of building out very strong enterprise sales teams,” says Malmberg. “They are really good at being at the intersection of technology and users – and being fast at picking up technology and offering it in a way that users want.”

Furthermore, in today’s volatile geopolitical climate, companies in strategically important sectors like manufacturing, energy and defense are also finding new levels of appetite from European governments who are seeing more need for sovereign technology.

“Because of what’s unfortunately happening in the world, it puts a sense of urgency to build up local supply,” says Malmberg. “Defense companies, and other businesses with a geopolitical USP, they’re now thriving in Europe because they have an urgent buyer they didn’t have before.”

Momentum shift

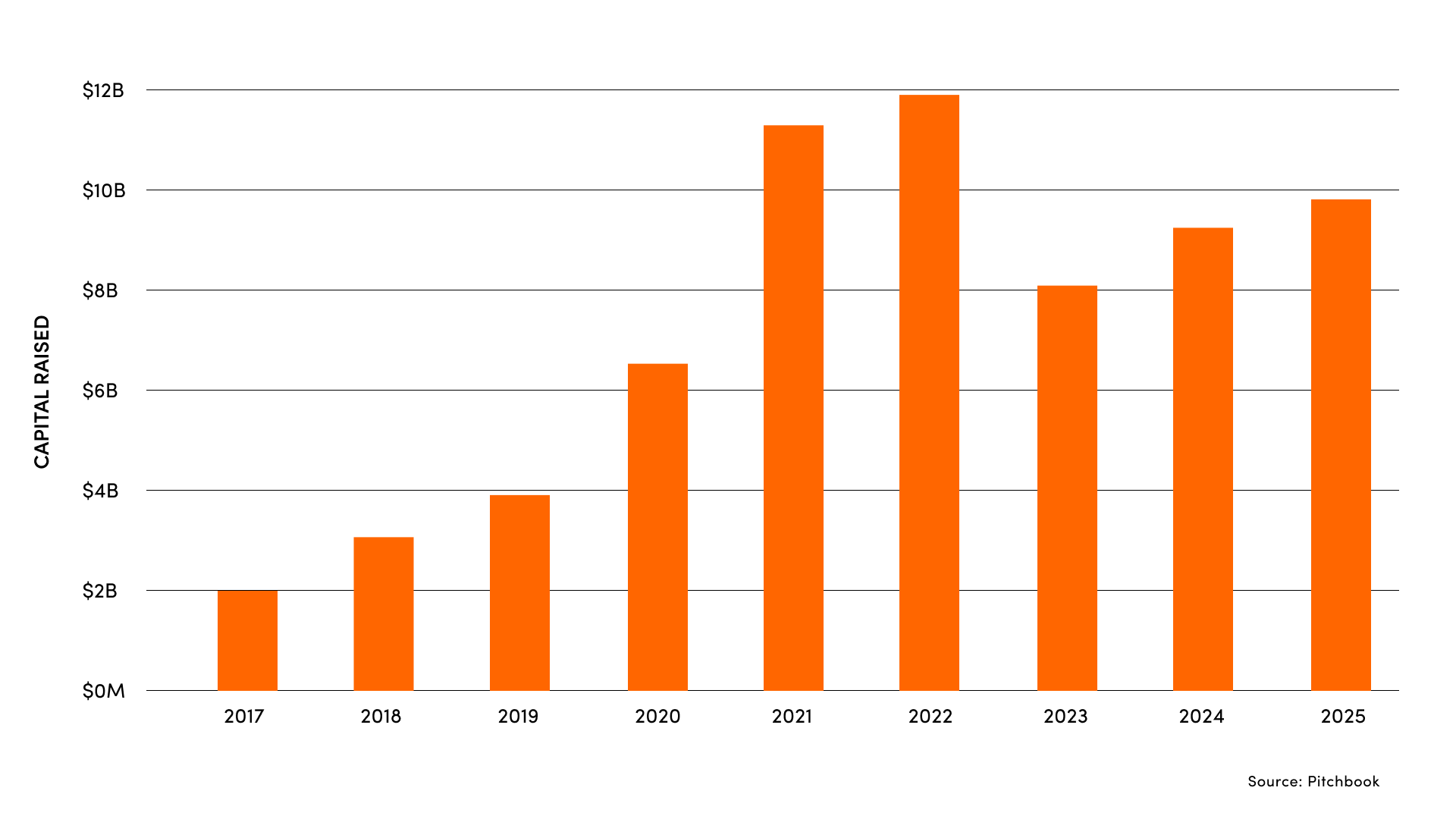

European companies, which have historically struggled to find local investors with the deep pockets to finance later-stage funding rounds, are also increasingly raising money from U.S. investors. In 2025, stateside firms poured $9.9bn into European tech companies, up from $2bn in 2017, according to data from PitchBook.

U.S. venture capital investment into European tech companies

Source: PitchBook

“There’s too little European later-stage capital, but there is later-stage capital in Europe. It just happens to come from U.S. funds,” says Malmberg. “European funds should own more and be a bigger part of the cap table for European companies.”

She adds that successful exits, such as Stockholm-based enterprise AI startup Sana’s $1.1bn sale to U.S. giant Workday, are another way that U.S. capital is helping to fuel the next generation of European tech.

“An important role of an exit like that is that you feed an ecosystem, so more people can become angel investors,” says Malmberg, adding that, until recently, a unicorn valuation was the ceiling of ambition for many in Europe. “That was a big target. Now we talk about decacorns or even more. Our ambition in Europe has just increased.”

ThinQ by EQT: A publication where private markets meet open minds. Join the conversation – [email protected]

Exclusive News and Insights Every Month

Sign up to subscribe to the EQT newsletter.