Michael Sidgmore: Private Markets Firms Need to Go Big or Go Niche

Michael Sidgmore is Co-Founder of Broadhaven Ventures and host of the Alt Goes Mainstream podcast. Here, he discusses the challenges private markets face heading into 2026.

Q: Michael, what are the biggest challenges private markets firms need to grapple with?

Michael Sidgmore: Alternative asset managers need to figure out who they are and what they want to be. My view is that firms will either need to be really big or really unique.

It’s worth noting that big in and of itself can be unique, as scale can be a differentiator, particularly in areas like infrastructure, real estate, secondaries, and private credit.

There are strategic questions that alternative asset managers will need to answer about their own business as the industry undergoes a period of consolidation and a move towards scale.

The first step? Look inward. Firms need to understand the unique edge and DNA that differentiate them from institutional and wealth channel investors, while also figuring out where to stay disciplined with fund size and strategy.

None of this will be easy. Firms that have aspirations to build multi-strategy platforms will likely acquire specialist managers to fill gaps in their platforms, even though this comes with the risk of diluting their own culture.

Additionally, firms will have to build and shape their narrative, or brand equity, to stand apart from peers. A clear narrative and brand will become a selling point to limited partners (LPs).

A key determinant of success will be the wealth channel.

Only certain firms have the investment strategy, deal flow, operational scale, and capital to build a business that can serve wealth channel investors. The larger the firm, the more likely they are to build and manage the evergreen structures that will become the delivery mechanism of choice to many investors in the wealth channel.

For those who favor specialization, a $5bn to $10bn AUM alternative asset manager can still be a great business and a fantastic investor. It will just mean differences in fund structures that a firm leverages, and also the types of LPs that a company considers its customers.

General partners (GPs) that are neither could struggle by being stuck in the middle – either too small to have the scale to win the wealth channel distribution game or too big to be different and unique.

Q: Distributions to investors suggest firms are still struggling to exit long-held holdings. What strategies are firms devising to ensure that investors get their money back, and are they working?

Michael Sidgmore: The past few years have been challenging for private market firms, particularly those in private equity. Exits have been scarce. The IPO market wasn’t really open, and many institutional LPs experienced the denominator effect, making it more challenging for them to allocate to new funds.

GPs have had to come up with ways to generate liquidity – some solutions which have been positive for the industry and some which have caused concerns for LPs.

The secondaries market has been one avenue for exits. Secondaries are forecast to be a $200bn global market by year-end (still only 1.5 percent of the total market size of private markets) and have become an attractive strategy for many LPs to generate liquidity in their portfolios.

Continuation vehicles (CVs) have become a popular innovation for GPs that have assets with runway to grow while also delivering liquidity to LPs waiting for distributions. A report from Schroders found that the CV market has grown at a 27 percent CAGR between 2013 and 2024 and will increase from $70bn in transaction volume to $300bn over the next decade.

But the rise of CVs has also led to questions about the quality of exits. Is private equity kicking the can down the road? And will these companies eventually have an IPO or trade sale?

The best solution? Invest in A-quality companies at appropriate entry prices that can exit when it makes sense.

Market Dynamics Driving Investor Interest in PE

Q: How is this liquidity blockage affecting the institutional LP outlook on private markets? Are LPs becoming more selective over who they invest with and why?

Michael Sidgmore: The lack of liquidity has undoubtedly impacted both institutional LPs and GPs.

For institutional LPs, a lack of exits meant that they have been overexposed to private markets the past few years relative to their public markets exposure. This feature has led to a structural challenge: institutional LPs have reached allocation limits in certain private markets strategies or funds, creating fundraising headwinds for GPs looking to raise net new capital from institutional LPs.

This structural challenge has created a qualitative conundrum for GPs when raising capital. Institutional LPs, facing lower levels of liquidity, have been forced to become even more discerning as to which GPs they decide to work with. There’s been a trend of doing more with fewer firms – across both fund commitments and co-investments. As a result, the bar for net new fund commitments has become increasingly high.

This feature of the market has also had a cascading impact on GPs and their business strategy. In some cases, large GPs have made the strategic decision to acquire or build capabilities in a different strategy, such as secondaries, private credit, or infrastructure, so that they can offer ways to expand the LP relationship into more products.

GPs have also had to figure out solutions to find additional co-invest capacity so they can keep deal volume in their own ecosystem and monetize that volume rather than syndicating it out to other GPs. In certain instances, that has resulted in building out wealth solutions businesses that can consume some of the co-investment capacity that would have otherwise been taken by institutional LPs.

The upshot? GPs need to ensure that their strategy and culture are aligned so that institutional and wealth channel investor relations teams can serve their respective clients well, and maintain relationships and increase wallet share of an LP even as the firm continues to evolve and grow its capital base and LP relationships.

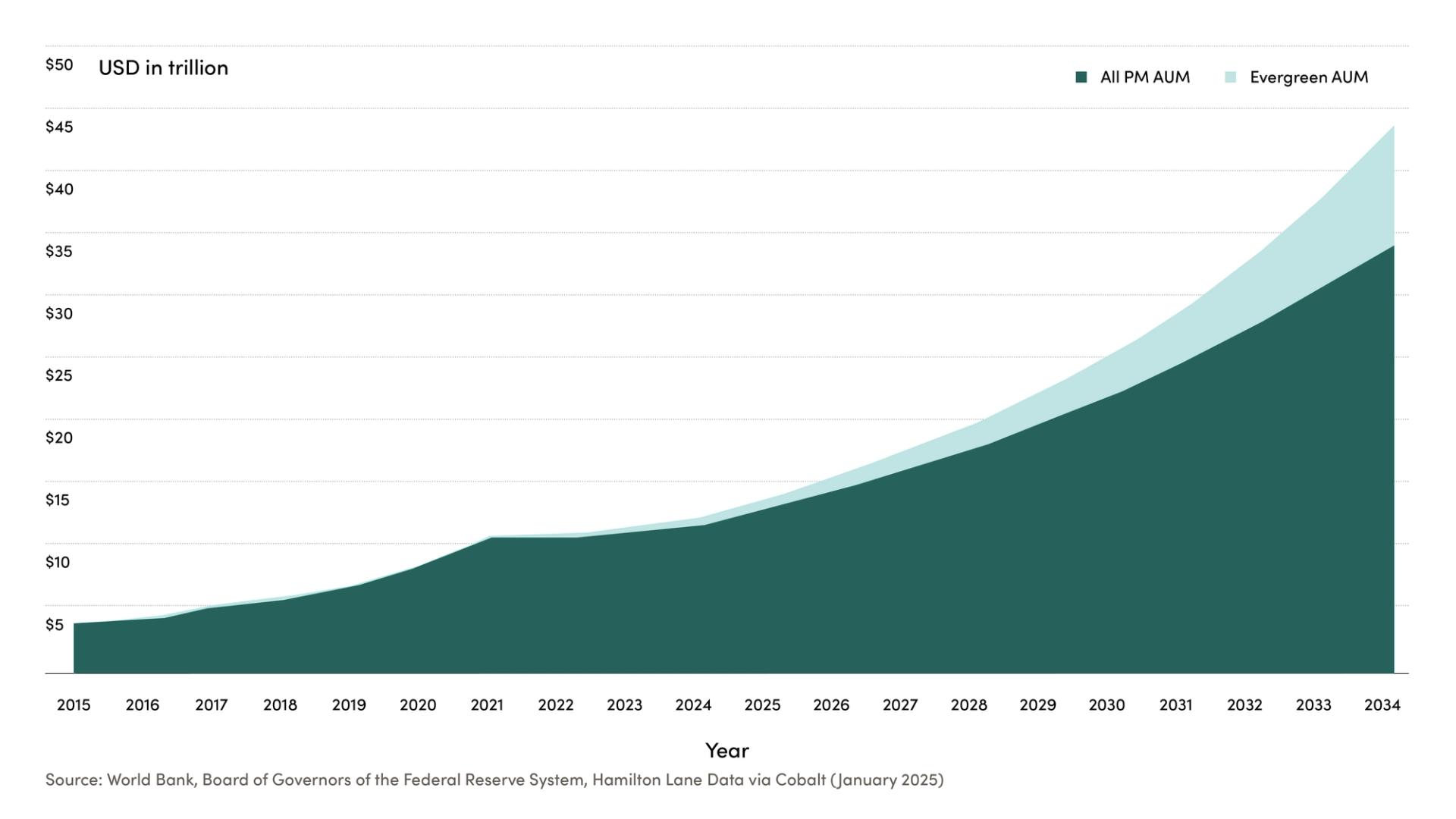

Q: Various forecasts expect a surge in private markets AUM over the coming decades, driven a lot by wealth channel money and evergreens. Based on your conversations with private markets firms, are people and companies prepared to handle this potential surge in available dry powder?

Michael Sidgmore: Is a GP equipped to handle an increased quantum of capital? The answer is it depends on the firm. The big question for GPs (and LPs doing diligence on a firm’s products) is whether or not the GP has enough deal flow to support its evergreen and closed-end funds.

Can GPs deliver on their promise of returns to LPs? As more capital comes into private markets, could returns go down? That’s certainly the fear – that more capital enters the space and returns decrease as more capital chases a finite number of deals.

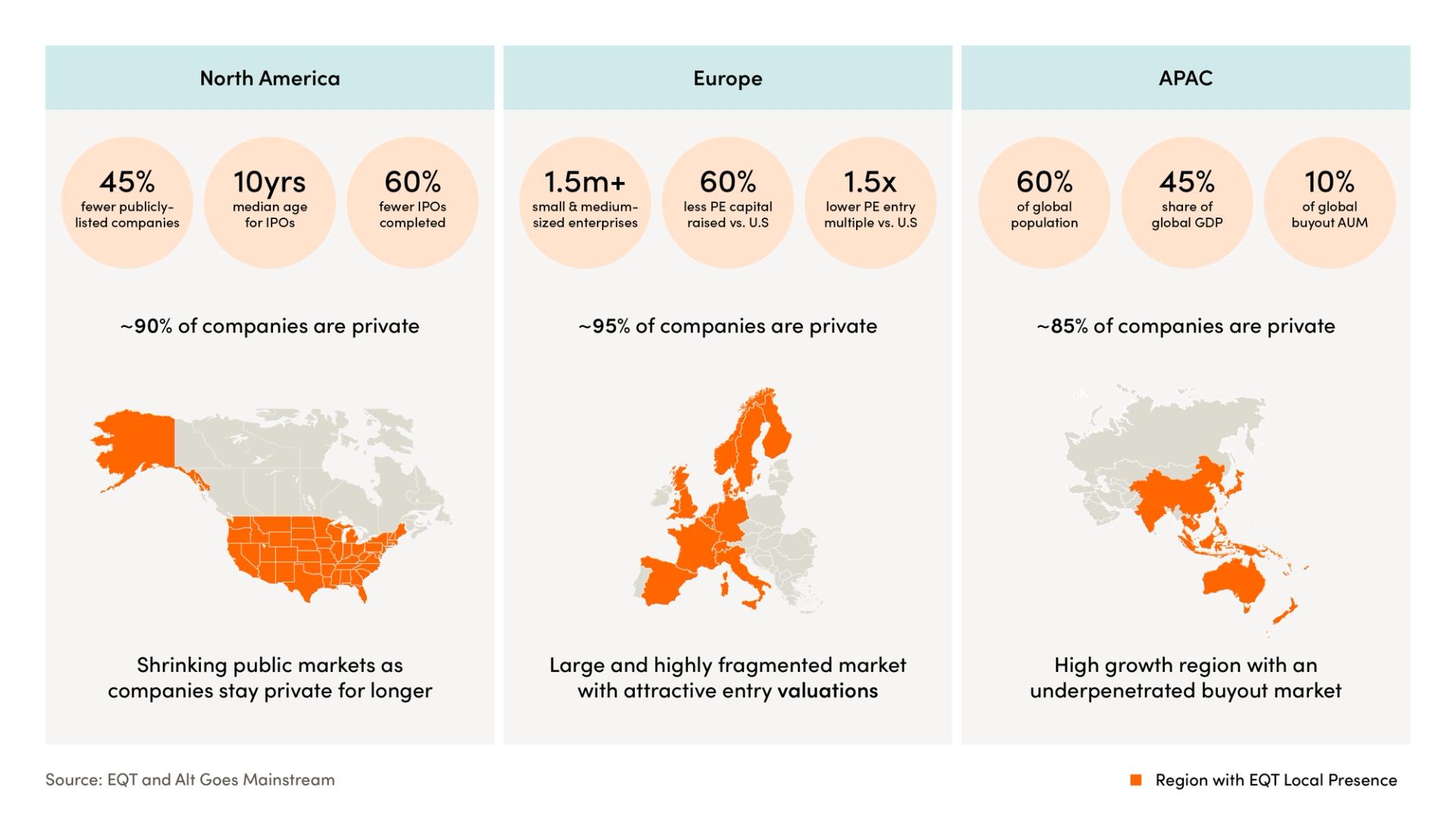

Proponents of private markets would likely make two arguments here: one, the indexation, correlation, and concentration in public markets mean that investors must at least consider private markets as a means of diversification and the possibility of increased returns. The second, that the vast majority of companies with $100m or more in revenue reside in private markets, meaning that there should be ample opportunity for private equity firms to invest in quality companies.

I do think that many GPs are being thoughtful and responsible about both of these questions. While many firms have an imperative to grow their own business and increase AUM, most recognize the responsibility that comes with working with the wealth channel. The responsibility only grows for firms that become providers to retirement and 401(k) channels. For the wealth channel to continue to allocate to private markets, returns must exceed public markets net of fees.

Predicted Growth of Evergreen AUM

Q: How will the pace of capital deployment be affected and will companies be able to maintain deal underwriting standards?

Michael Sidgmore: GPs must maintain discipline around underwriting standards and capital raising efforts, particularly with evergreen funds.

It will be critical for GPs to limit inflows into evergreen funds to appropriate levels based on how many deals they can originate and are mindful of how additional inflows could impact returns and NAV.

Different GPs will have differing goals and mandates based on the size of their fund, so there’s no one right answer to this question, but maintaining discipline will drive outcomes.

Q: How do you delineate the different wealth channel routes firms are taking?

Michael Sidgmore: The wealth channel is not monolithic. Different cohorts within the wealth channel are seeking different solutions and require differing levels of operational support from a product and investor relations perspective.

To do wealth at scale, asset managers must do a number of things exceptionally well:

- Manufacture products that meet the needs of the different segments of the wealth channel.

- Invest in educating the wealth channel, which means they need to build out marketing and distribution capabilities.

- Have distribution “boots on the ground” to cover, serve, educate, and communicate with investors if they want to work with private banks, wirehouses, broker dealers, and large portions of the independent wealth management community.

Q: With all the talk of evergreens, does the drawdown fund still have a future?

Michael Sidgmore: Long live the drawdown fund. The demise of the drawdown fund is greatly exaggerated. Though large portions of the wealth channel will utilize evergreens for ease of use and access to private markets, many institutional investors and some wealth channel investors might choose to stick with drawdown funds – or employ a core (evergreen) and satellite (drawdown) approach to asset allocation within private markets.

Smaller GPs can take solace in this aspect of the industry evolution. They might be able to differentiate in distribution by having a drawdown fund rather than an evergreen fund and lean into fund size, specialization, and velvet roping.

Q: Do you expect retail investors to have any impact on how private market managers disclose information and operate, or will it be a case that if you want to invest in private markets, you need to accept how we do things here?

Michael Sidgmore: Yes, the industry is already seeing an evolution in reporting and transparency. This is particularly the case in interval funds that have a daily ticker. Many evergreen funds report on a monthly basis – and some on a daily basis. These requirements mean that funds must disclose information on a more frequent cadence.

We know from public markets that incentives drive outcomes. When public companies are on a quarterly reporting cycle, sometimes they manage their business to impact quarterly earnings and stock price. Will the more frequent reporting cadence of evergreen funds drive how managers underwrite, invest, and manage evergreen fund portfolios?

I imagine that just like how the best public companies manage to deal with shorter reporting cycles while maintaining a long-term outlook, so too will the best evergreen fund managers. It does give rise to the question of what skillset is required to best run and manage an evergreen fund. Perhaps GPs that have run evergreen fund strategies will have to either acquire or build different skillsets and competencies than they had with drawdown fund structures.

It’s also worth noting that the possibility of private market products being included in 401(k)s will likely have an impact on reporting and disclosure. Part of the impediment to date with bringing private markets exposure into 401(k) accounts has been reporting and disclosures. That could change as evergreens continue to develop a performance track record.

The views expressed in this publication are the personal views of Michael Sidgmore and do not necessarily reflect the views of the EQT AB group ("EQT") itself or any investment professional at EQT.

Michael Sidgmore is Co-Founder and Partner at Broadhaven Ventures, a principal investment group that invests in fintech and private market tech companies, funds, and helps build asset management businesses, including Cantilever, a GP stakes fund. Broadhaven Ventures is affiliated with financial services investment bank Broadhaven Capital Partners. Michael is also the founder of the Alt Goes Mainstream podcast, where he interviews senior leaders from the private markets industry and writes a weekly newsletter on the industry.

ThinQ by EQT: A publication where private markets meet open minds. Join the conversation – [email protected]

On the topic ofOpinons

Exclusive News and Insights Every Month

Sign up to subscribe to the EQT newsletter.