What is Private Credit?

The private credit market has exploded since the global financial crisis, as traditional banks cut back on riskier corporate lending. Private credit funds stepped in, funded by institutional investors seeking asset diversification and steady, debt-like returns.

- Private credit is lending to companies by institutions other than traditional banks – from specialist asset managers to private equity firms

Private credit is a type of lending by financial institutions that are not banks, such as alternative asset managers and private equity firms. Also known as private debt, direct lending or private lending, it has become one of the most consequential forces reshaping how businesses around the world access capital.

Private credit funds raise money from investors, then make loans directly to businesses, rather than buying equity in them. Those loans are typically due for repayment after three to seven years and usually carry a floating (variable) interest rate, meaning returns adjust as the interest rate environment shifts.

Businesses that find it hard to borrow in more traditional ways, such as from banks or the corporate bond markets, often turn to private credit. This might be because they don’t meet strict bank lending criteria, need more flexible terms than public markets can offer, or simply want faster execution certainty.

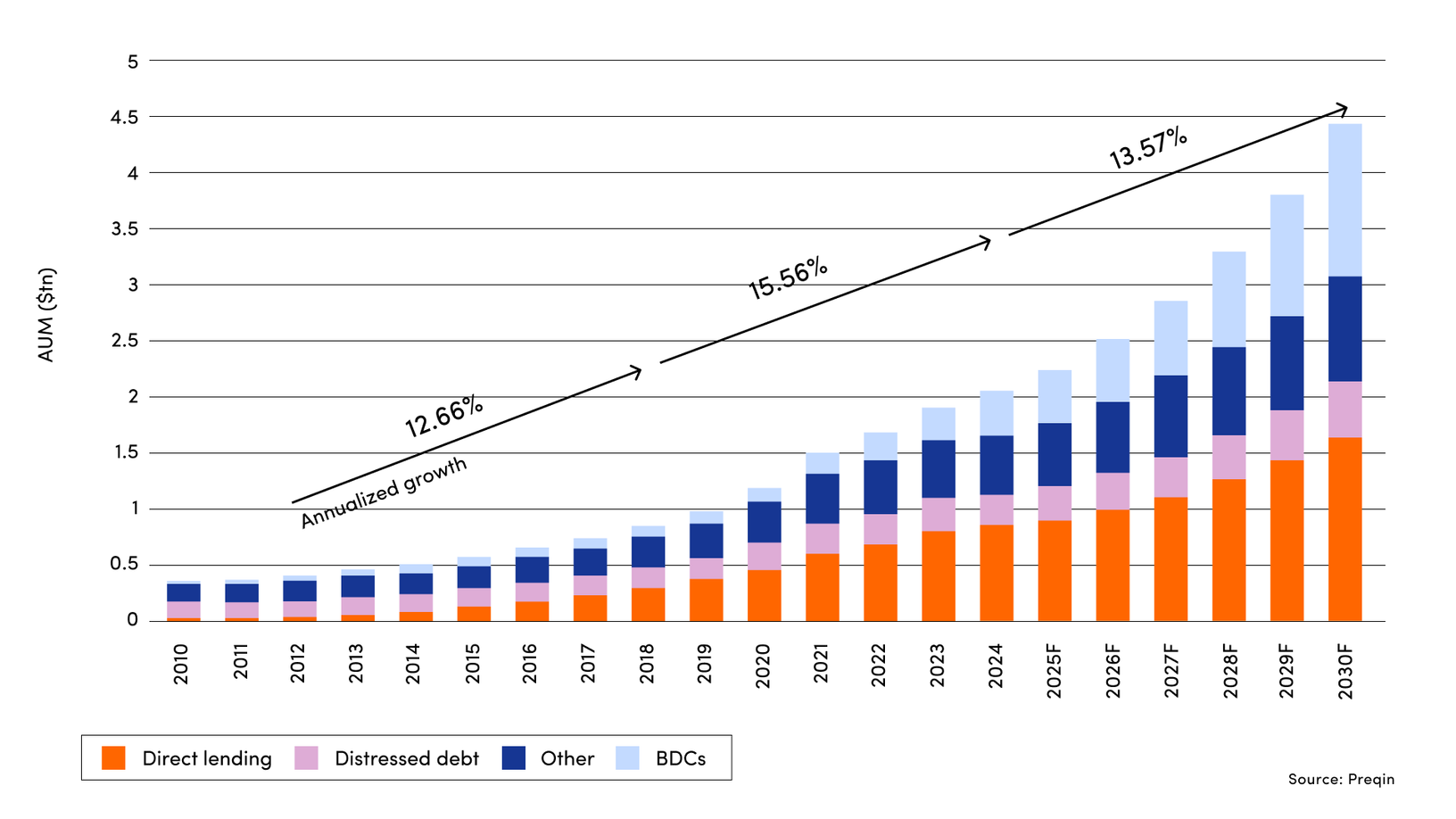

Private credit has exploded since the global financial crisis in 2008-9, when banks cut back on lending, and investors sought yield in a zero-interest-rate environment. The worldwide market has grown from around $230bn in assets under management in 2008 to around $2.3tn in 2025, according to Preqin. It is estimated to grow to $4.5tn by 2030.

Private credit AUM estimated to double by 2030

That growth has been accompanied by a surge in deployment: private credit capital deployment grew to $592.8bn in 2024, up 78 percent on 2023 volumes, according to the Alternative Credit Council (ACC).

Roughly 65 percent of private credit fund AUM invests in the U.S., but Europe is catching up fast, according to ACC data. The continent now accounts for close to 30 percent of global private credit assets under management, with particularly strong growth dynamics across mid-market lending and infrastructure finance.

The attractions of private credit for a portfolio

Pension funds, family offices, insurance companies, high-net-worth individuals, and sovereign wealth funds are among the biggest investors – known as limited partners – in private credit funds.

Private credit is used by institutional investors for its low correlation with public markets and portfolio diversification, especially as the range of private credit assets available has rapidly grown in recent years.

For example, while private credit was typically extended to mid-market firms with annual revenues between $10m and $1bn, this has now changed to include larger companies, spreading credit risk across a wider range of businesses.

Today, private credit lends across an enormous range of borrower types and deal structures: corporate direct lending, infrastructure debt, venture debt, commercial real estate debt, and increasingly, asset-backed finance. This breadth of exposure means private credit funds can potentially construct portfolios with exposure across a range of borrower types and asset classes, less correlated with public markets or macroeconomic swings.

Private credit comes to Main Street

Perhaps the most significant shift underway is one that barely existed a few years ago: private credit is opening up to eligible individual investors.

Historically, access to private credit required institutional scale, minimum tickets of $5m or more, long lock-up periods, and complex reporting. New fund structures, most notably evergreen funds, are changing that equation. Unlike traditional drawdown funds, evergreen structures allow continuous capital deployment and provide redemption opportunities at set intervals, making them potentially more compatible with the way individual investors generally manage their money.

The results are already visible with private credit evergreen funds surpassing $700bn in AUM by the end of 2025.

Regulation is accelerating the shift. In August 2025, the Trump administration signed an executive order opening America’s $12.5tn defined contribution pension market, including 401(k) plans, to private market investments.

That said, the democratization of private credit comes with important caveats. The structures designed to bridge the liquidity mismatch, including quarterly redemption windows and NAV-based pricing, are largely untested under conditions of real market stress. Investors considering private credit allocations should understand that periodic liquidity is not guaranteed liquidity and that valuation methodologies in private credit are fundamentally different from marked-to-market public securities.

The road ahead

Private credit has spent the better part of two decades expanding across market cycles, expanding its borrower base, and broadening the range of assets it can finance. The next phase, serving individual investors at scale, partnering with banks rather than competing with them, and lending against an increasingly diverse range of assets, is already underway.

The defining question will be whether the industry can maintain the underwriting discipline and investor transparency that built its reputation during a period of rapid growth and structural change. As the asset class moves from institutional niche to mainstream allocation, the standards by which it will be judged are getting higher.

ThinQ by EQT: A publication where private markets meet open minds. Join the conversation – [email protected]

More Essential Reads

Exclusive News and Insights Every Month

Sign up to subscribe to the EQT newsletter.