Why Pension Funds Invest in Private Equity and What It Means For U.S. Savers

Pension funds are trusted to invest and grow the savings of millions of ordinary investors to provide them with an income in retirement. Private equity can play an important role in diversifying the assets of these funds with the potential to provide long-term, stable returns.

- Pension funds are often large, institutional investors that invest on behalf of people who are saving for retirement.

A pension fund is an investment vehicle that takes in money from workers who are specifically saving for their retirement. A pension fund invests this money with the aim of growing it to provide savers with an income that can be drawn once they reach retirement age.

Pension funds hold, manage and invest very large sums collectively on behalf of retirement investors. They invest in a range of assets – including company shares, bonds, real estate, commodities, and private equity (PE). Pension funds are for long-term investors, investing with a time horizon of decades, in line with restrictions on at what age investors can access their money.

The Global Pension Assets Study in 2026 estimated that $68.3tn was held in global pension fund assets across 22 major pension markets, equivalent to 74 percent of the GDP of those economies.

One type of pension fund is the institutional investor, which has professional management teams and an influential role in the global investment landscape. They fund a wide range of large-scale projects, companies and governments globally.

The world’s largest such pension fund is Norway’s Government Pension Fund with $1.77tn under management. Another example of an institutional investor pension fund is the California Public Employees’ Retirement System (CalPERS), which has more than $500bn in assets.

Another type of retirement plan is the self-directed pension fund, such as the U.S.’s 401(k), where individual account holders get to pick and choose which assets to own. Recent rule changes may make it easier for such accounts to also invest in private markets assets including PE.

Overall, the U.S. remains the largest pension market, followed, at a significant distance, by Canada, Japan and the UK. These four markets account for 81 percent of pension assets in the largest 22 pension markets, according to the study.

How pension funds invest

Pension funds rely on inflows from employers and their employees, who usually pay a monthly contribution deducted from their salary. The pension fund manager then pools the capital to buy assets on the savers’ behalf. Each investor owns the assets held in their own account, but, for the purpose of investing, all investors’ money in the fund is pooled.

A pension manager’s goal is to pick investments that will grow over time. This could be through increases in the share prices of the companies the fund invests in, dividends from shares, rents from real estate, or interest earned on fixed-income assets like bonds. Returns are not guaranteed, but generally investing in pension funds over a long period is more likely to increase the value of savings versus holding the money in cash, which generally depreciates against inflation.

The pooled nature of an institutional investor pension gives the fund’s manager more buying power overall – meaning access to more investment opportunities, including PE, than an average worker would typically be able to get alone.

Pension fund allocation to private market assets

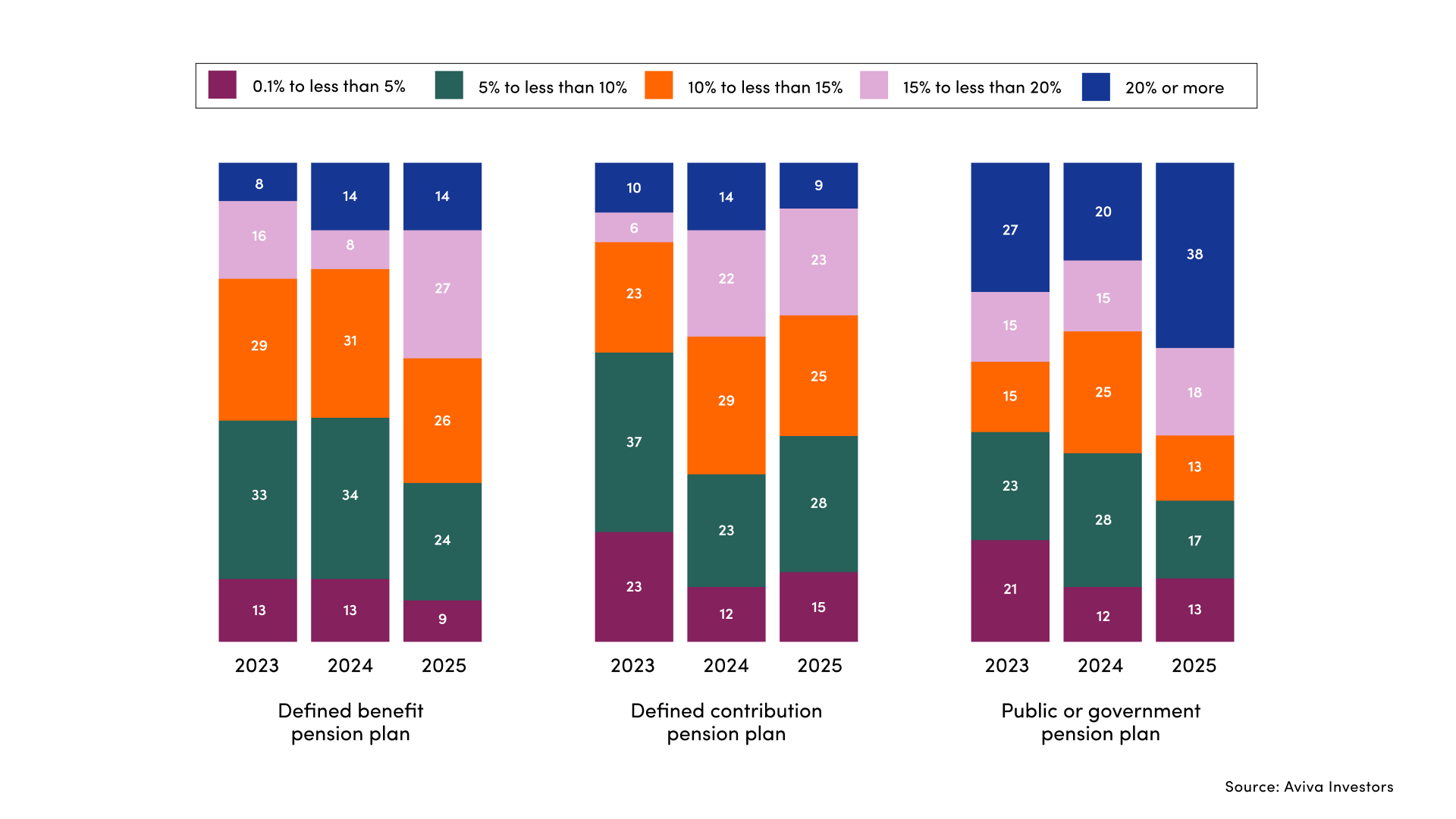

The combination of asset size and long term investment horizon has made them significant investors in PE: a 2025 study by Aviva Investors found that more than half of global pension funds allocated at least 10 percent of their portfolios to private markets, a category that includes private equity and other private strategies, such as private credit. At least one third of pension funds had a weighting of 15 percent or more in private assets.

CalPERS, for example, held $98bn of its asset pool in PE investments as of mid-2025. In 2024, CalPERS raised its PE allocation from 13 percent to 17 percent of its total portfolio.

Why pension funds invest in private assets

Because people paying into pension funds often aren’t able to access their money for many years, even decades, pension vehicles are able to lock up a significant minority of their assets in funds that hold illiquid assets, like PE, without worrying about near-term liquidity demands. The pension funds hope to benefit from above public-market returns generated by privately held companies that are often improved by PE managers as part of a value-creation strategy.

Institutional pension funds began investing in PE in North America in the late 1970s to diversify into “non-traditional” asset classes, against a backdrop of weak performance of their more traditional investments in listed equity markets. The period of low interest rates from 2010 to 2022 pushed more pension funds to pursue a search for yield, with them increasingly turning to private equity.

Further shifts may be coming as governments make it easier for self-directed pension funds to invest in private markets. The U.S. recently relaxed rules so it will be easier for certain self-directed pensions, including 401(k)s, to hold private markets funds. The UK and European Union have adopted a similar stance. A 2025 Apex Group survey found that 67 percent of retail investors are now interested in including PE in their portfolio, citing diversification as their primary driver. This is expected to be a significant source of new inflows into private market funds in the years ahead.

ThinQ by EQT: A publication where private markets meet open minds. Join the conversation – [email protected]