What Is a J-curve?

What a J-curve could teach you about investing

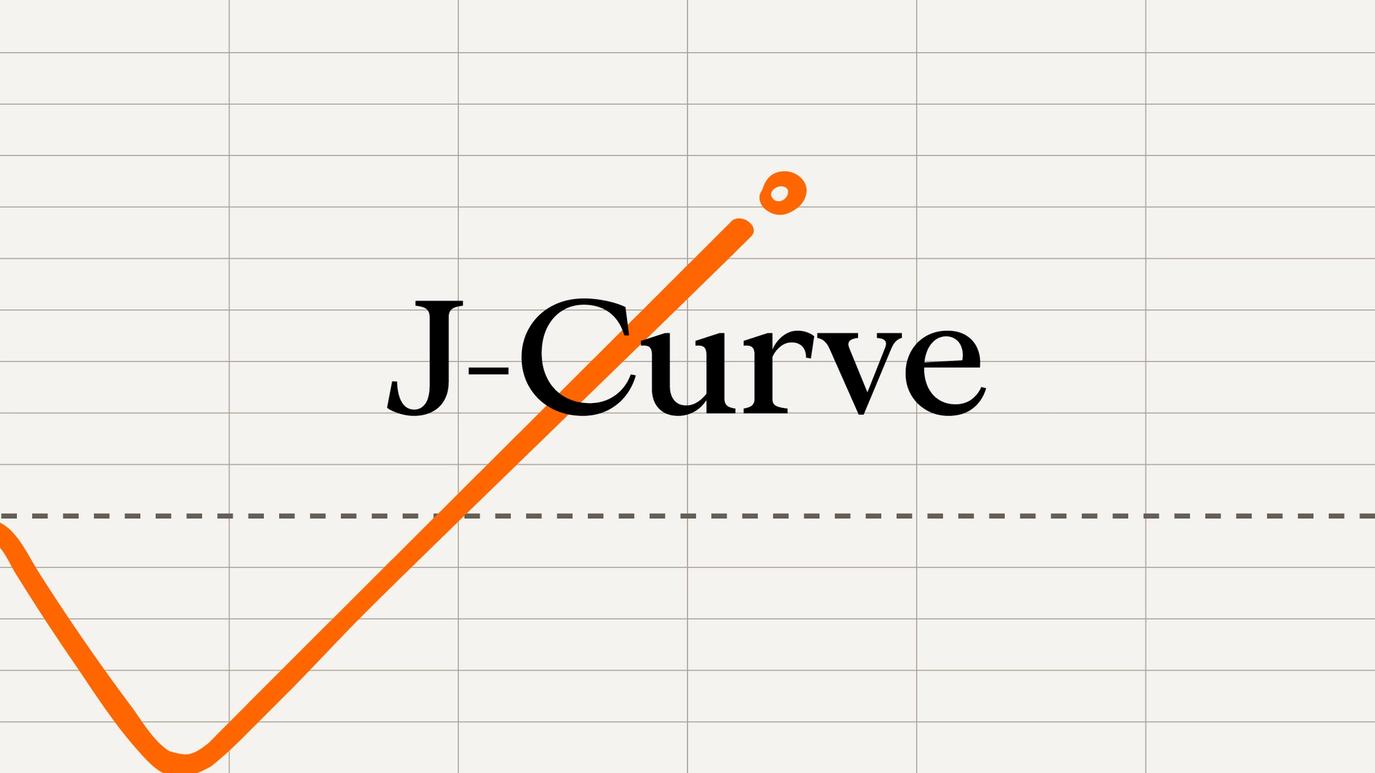

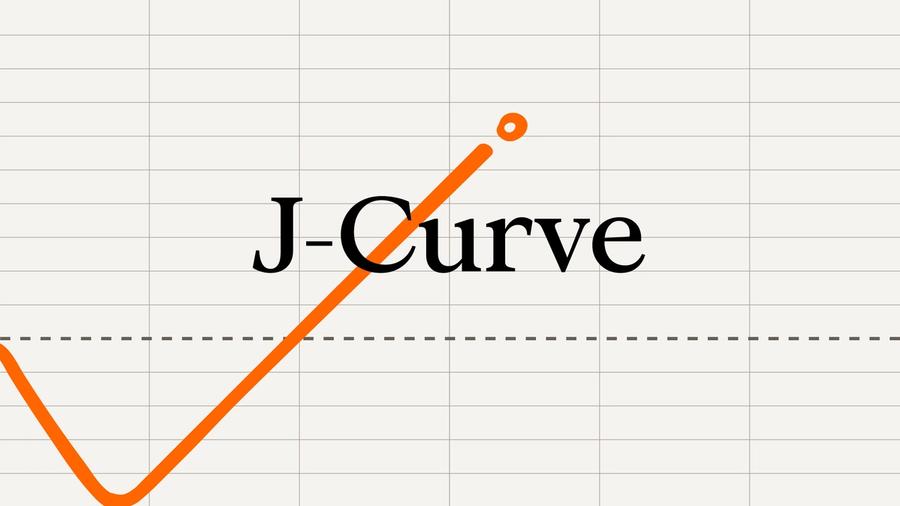

- A J-curve describes the typical return trajectory of a private equity fund.

The term “J-curve” refers to a pattern on a chart where the value of an investment initially falls before eventually climbing above its starting point – tracing the shape of the letter J. It is used across economics and finance to describe a range of phenomena that follow this dip-then-rise pattern.

For a private equity fund, the J-curve describes the expected trajectory of investor returns over the life of the fund. In the early years, returns are typically negative. As the fund’s investments mature and begin to generate value, performance improves. In a successful fund, returns eventually climb well above the original investment, creating the upward sweep that completes the J.

Why does the dip happen?

The initial downward movement in a PE fund’s performance is not a sign that something has gone wrong. It is a natural consequence of how the asset class works, driven by several overlapping factors.

Fees come before returns: From the moment a fund is raised, the general partner (GP) begins charging management fees, typically around 1-2 percent of committed capital per year. In the early years of the fund, before any investments have been made, these fees are being paid out while the portfolio has yet to generate any value. The effect is to push the net return into negative territory from the outset.

Capital is deployed gradually: PE funds do not invest all their capital on day one. The investment period typically spans three to five years, during which the GP sources, evaluates, and acquires companies. Capital that has been committed but not yet called is not generating a return, and the assets that have been acquired are at the earliest, and often lowest-value, stage of the investment cycle.

Early-stage investments are carried at cost or below: When a PE firm first acquires a company, it will often make significant upfront investments in transformation – restructuring operations, replacing management, investing in technology, or repositioning the business strategically. These improvements take time to show up in the company’s financial performance and, in the interim, the asset may be valued at or below its purchase price.

Why performance recovers

The upward arc of the J begins to emerge as the fund’s investments mature and value creation work starts to bear fruit.

As portfolio companies grow revenues, expand margins, enter new markets, or complete strategic acquisitions, their valuations rise. The GP begins to exit investments, returning capital to investors. These distributions hopefully drive the fund’s net return from negative into positive territory and, in successful funds, well beyond.

Understanding the J-curve is important for private equity investors because it demonstrates that investments often take years to generate significant profits – if at all.

They allow investors to set realistic expectations for when and how returns may materialize, emphasizing the importance of a long-term commitment. Investors must be prepared for early losses during the early stages of their investment, and the J-curve highlights the need for patience and strategic planning to achieve desired returns.

ThinQ by EQT: A publication where private markets meet open minds. Join the conversation – [email protected]